Start a new quote

New customer to Sun Coast? You are in the right place. Select a product below to get started.

New customer to Sun Coast? You are in the right place. Select a product below to get started.

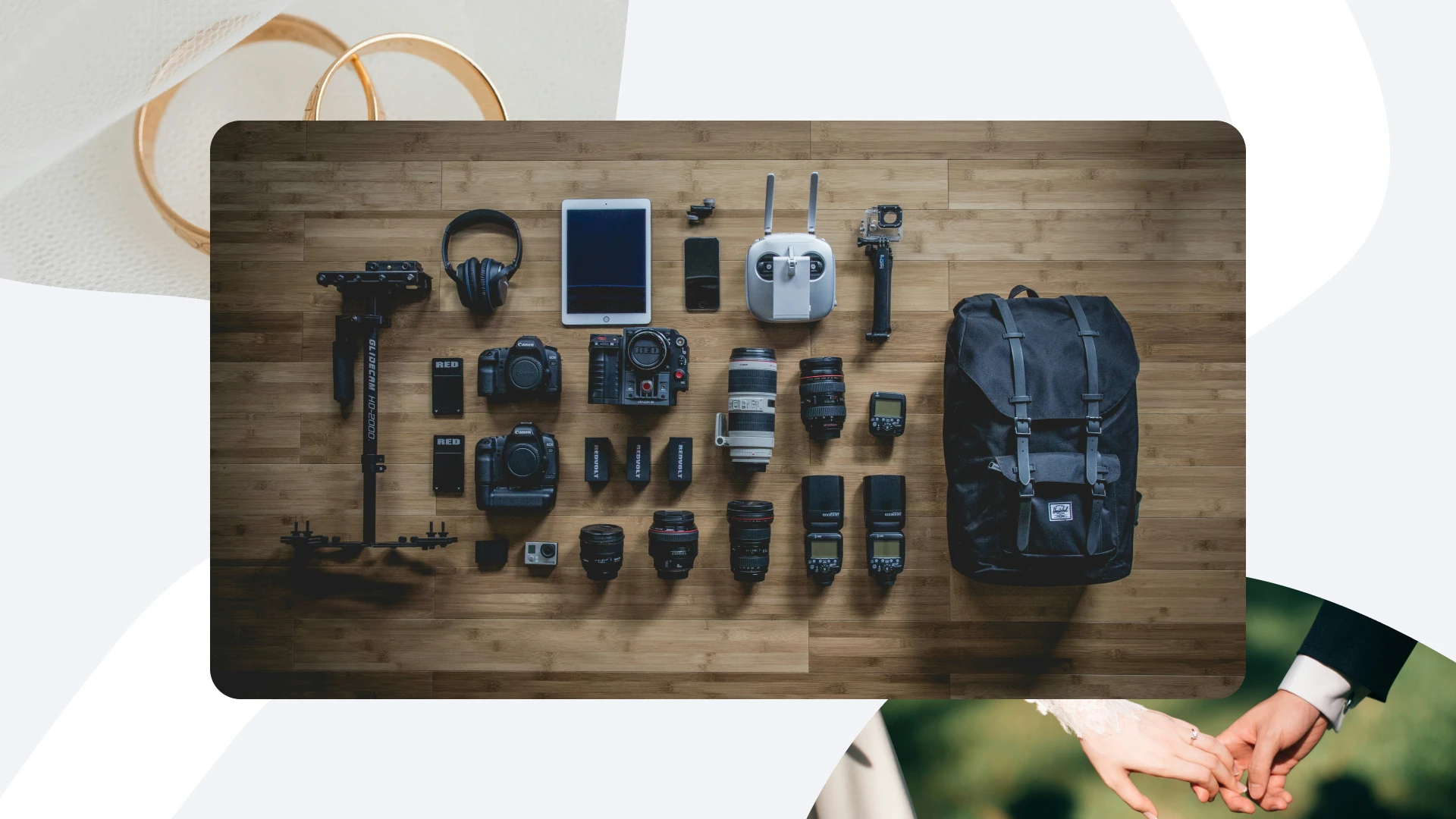

If you own expensive photography equipment, you may assume your homeowners or renters insurance automatically covers it. In some cases, that’s true — but how you use your gear and where the loss occurs can make all the difference.

Homeowners & Renters Policies

If your camera is stolen while shooting a family vacation, a homeowners claim might be paid (up to policy limits and deductibles).

If the same camera is stolen during a paid wedding shoot, the claim could be denied if your policy excludes business use. This is a common issue for side-hustle creatives, which is why this article on insurance for part-time or freelance wedding photographers is worth reviewing.

Even for personal-use coverage, your homeowners policy may have:

Coverage may not apply if the loss happens:

Venue rules can also affect coverage expectations, as outlined in this article on whether you need insurance to photograph at certain venues.

If you’re a professional or semi-professional photographer:

In addition to gear protection, many photographers also consider professional liability insurance to help address client claims related to errors, omissions, or missed deliverables.

Disclaimer: This article is for general informational purposes only and is not legal or insurance advice. Coverage availability, terms, limits, and exclusions vary by insurer, policy, and location. Always confirm with your insurance provider whether your gear is covered in the situations you need.